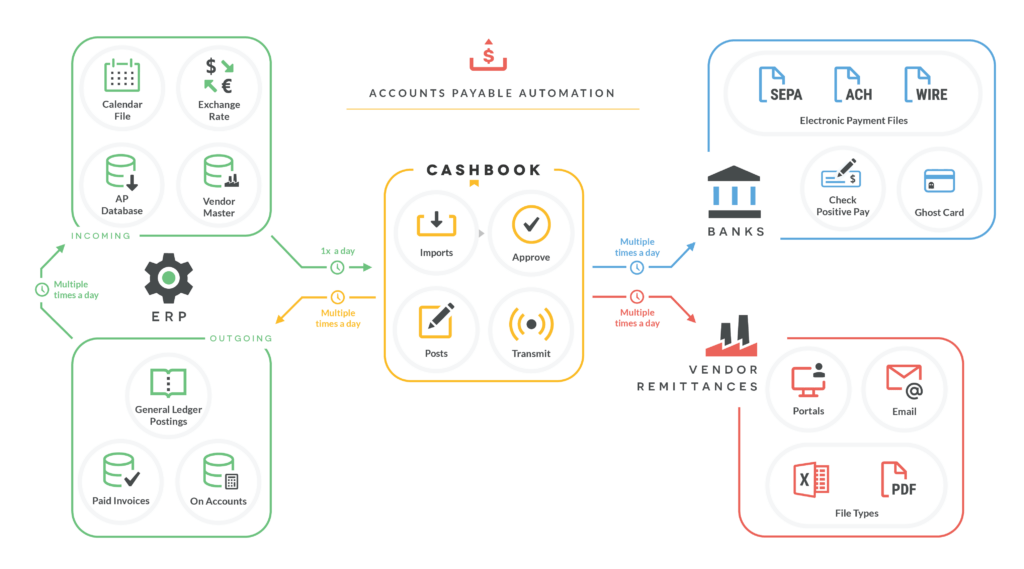

Streamline Payments with Cashbook’s SEPA Application

What Is SEPA?

Cashbook Migration Pack or SEPA Credit Transfers (SCT)

The Single Euro Payments Area (SEPA) is the payments integration initiative of the European Union for simplification and harmonisation of bank transfers. As of March 2012, SEPA consists of the 27 EU Member States, plus the four members of the EFTA (Iceland, Liechtenstein, Norway and Switzerland) and a remaining country, Monaco.

Key Objectives:

The project’s aim is to improve the efficiency of cross border payments and turn the fragmented national markets for Euro payments into a single domestic one. SEPA will enable customers to make cashless Euro payments to anyone located anywhere in the area, using a single bank account and a single set of payment instruments. The project includes the development of common financial instruments, standards, procedures and infrastructure to enable economies of scale.

SEPA Deadline: 1st of February 2014

Since January 2008, SEPA credit transfers and direct debit transfers have been in operation. Euro States must migrate to the SEPA standards before the SEPA migration end-date of the 1st of February 2014 & Non Euro States for the 31st of October 2016.

Which currencies are eligible for SEPA?

Euro currency transactions only.

Background to SEPA

Prior to SEPA there were many different payment areas or ‘clearing systems’ within Europe. This resulted in cross border European payments being both expensive and disparate. The European Payments Council (EPC) has laid the groundwork for a more standardised payment infrastructure.

Features

- Configurable SEPA format that can fit to any bank.

- Flexibility in ERP data exports into the SEPA format.

- Email Remittance capability and PDF creation.

- IBAN validation and IBAN file import with data cleansing.

Benefits

How your business will benefit from SEPA Credit Transfers (SCT):

- A customer involved in a Credit Transfer payment can only be charged by their own payment service provider.

- Facilitates lower transaction charges for payments across SEPA Zone from a single Eurobank account.

- 140 characters of remittance information are delivered without alteration or omission from the payer to the payee.

- Easy identification of a payment through specific data fields which clearly indicate payment types (i.e. salaries or taxes).

- Pre-agreed timeframes for delivering Credit Transfers provide certainty for cash collection.

- Facilitates automatic reconciliation of incoming payments with outstanding invoices basedon the ISO Creditor Reference Standard (ISO 11649).

The EPC believes that SEPA has a number of benefits including:

- All banks offer the same type of product and adopt the same format.

- Equal time limits, equal fraud-risk levels and equal processes across the Euro Zone.

- Reduction of costs of electronic money and payment transfers.