November 19th, 2020

Check stock is dead, long live the 3rd Party Check

To borrow from the great Mark Twain, reports of the demise of the check are greatly exaggerated. This payment instrument continues to enjoy immense popularity. Especially in North America within the Small to Medium Business (SMB) and Business to Consumer (B2C) sectors. However, it’s true that digital is the future.

The payments landscape will continue to shift toward digital payments, as service providers continue to innovate and make it easier and cheaper to go digital. However, the humble check has also benefitted from innovation even as it continues to lose popularity as a payment instrument. (Federal Reserve Payments Study)

The 3rd party check model

A service quickly gaining in popularity is the 3rd party payment provider model. This service entails that the bank or other financial services provider, issues checks on behalf of their clients. This is a fully outsourced Accounts Payable check service, where the issuing entity prints, posts and settles checks against an internal clearing account. Essentially, finance and accounting can avoid holding a stock of checks.

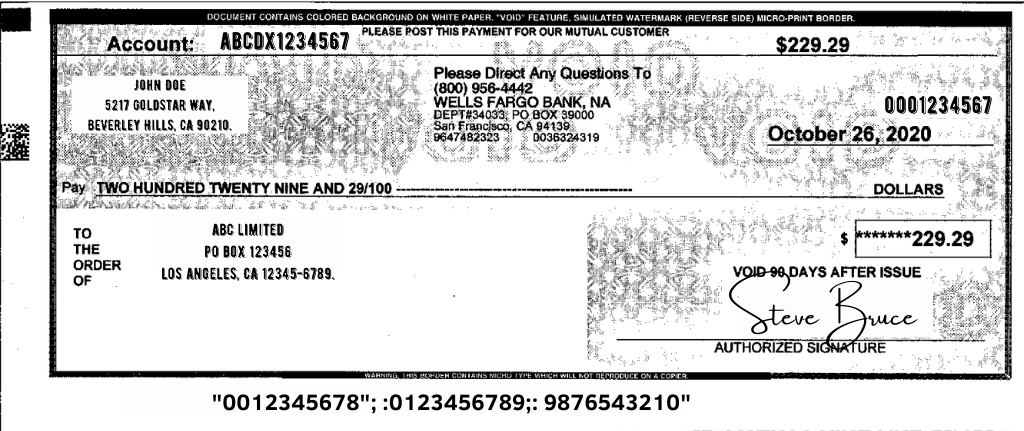

There are several impacts on the Accounts Receivable process from this outsourced payment service. For the recipient of the funds, the check might be issued by a bank such as Citi, Wells Fargo or Sun Trust. Several Accounts Receivable checks will arrive with the same payer account in the MICR (Magnetic Ink Character Recognition). Usually the original payer is referenced at the top of the check by name and/or customer number. There is typically no other remittance information, although the bank may provide a reference line on the check capable of listing a few invoice numbers.

Cashbook and the 3rd party payment provider model

Whether these payments are received directly or through a lockbox service. Cash Application automation requires a different process to that normally used for checks issued by customers and accompanied by remittances. Cashbook has developed a specialized cash application process for these checks that circumvents the need for any customer-built templates. Intelligent OCR is used to identity the customer from the check. We then apply the cash automatically using a series of matching algorithms that cater for high-probability payment scenarios.

As banks continue to push and grow their check services. We expect that cash application teams will see a move away from customer issued checks toward 3rd party checks. Cashbook’s Cash Application users will benefit from the automation process around this particular check type. They will get higher and higher automation levels as handwritten checks are increasingly replaced by this payment service.

Checks will continue to be around for the foreseeable future. Even as banks and other providers automate the needs of their SMB and B2C client base. There is life in the old check yet, especially as providers continue to innovate around this trusted and most familiar payment instrument.